The first time someone explained to me that I could make money by connecting businesses to lenders — without risking a single dollar of my own — I thought there had to be a catch. There wasn’t. But getting to the point where that model actually worked took longer than I expected, and the mistakes I made along the way were completely avoidable.

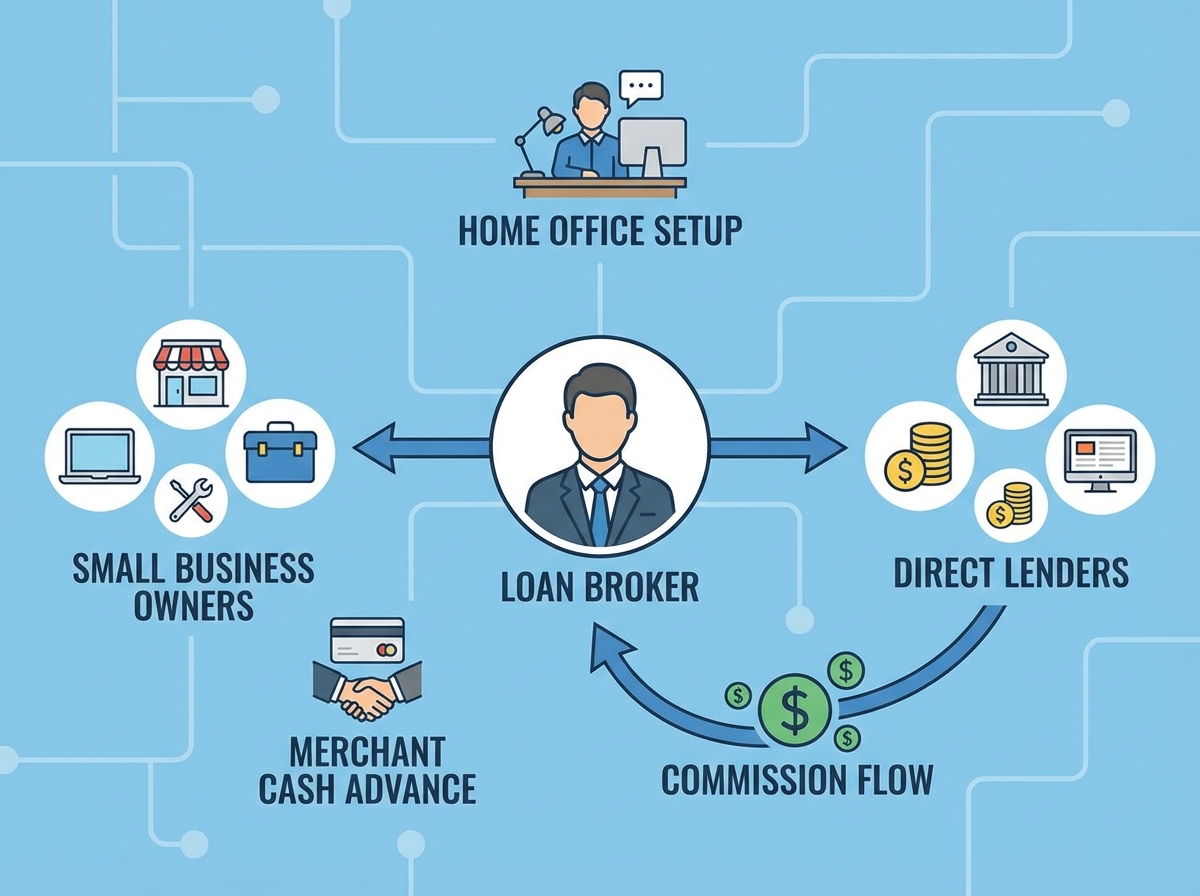

If you’re looking to learn how to become a business loan broker, the short answer is this: you act as an Independent Sales Organization (ISO), finding small business owners who need capital, then connecting them to direct lenders who fund the deal. You earn a commission from the lender after the business gets funded. No personal capital required. No license required in most cases. The entire operation can run from a laptop.

- You don’t need sales experience to start — but you do need a system for finding business owners who are actively looking for funding

- The biggest income lever isn’t your close rate, it’s your lead volume — which is why marketing comes before sales in this business

- Merchant cash advances fund faster than traditional loans (sometimes within 24 hours), which means your commission timeline is shorter than almost any other financial product

What a Business Loan Broker Actually Does

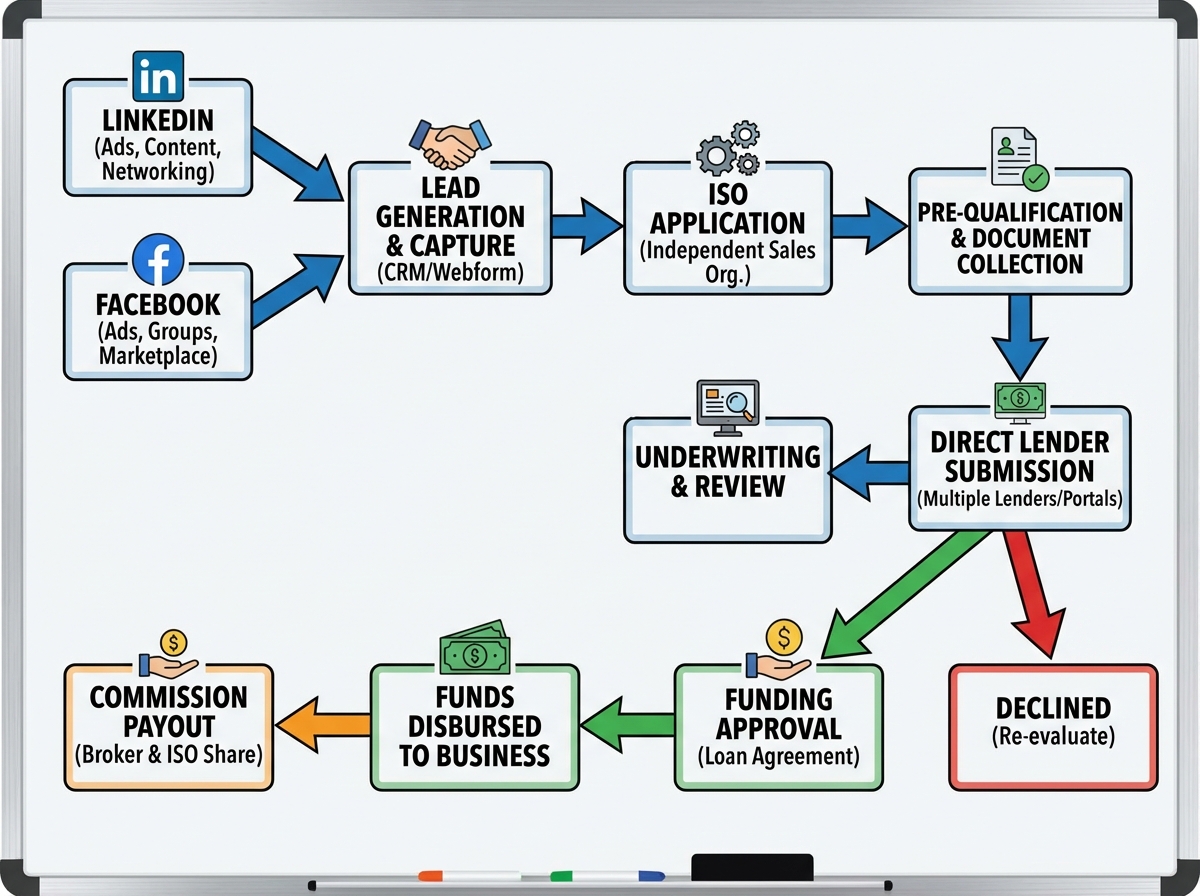

A business loan broker — sometimes called an ISO, or Independent Sales Organization — sits between small business owners who need capital and the direct lenders who provide it. You don’t lend your own money. You don’t underwrite risk. You identify a need, qualify the business, submit the application to a lender, and collect a fee when the deal closes.

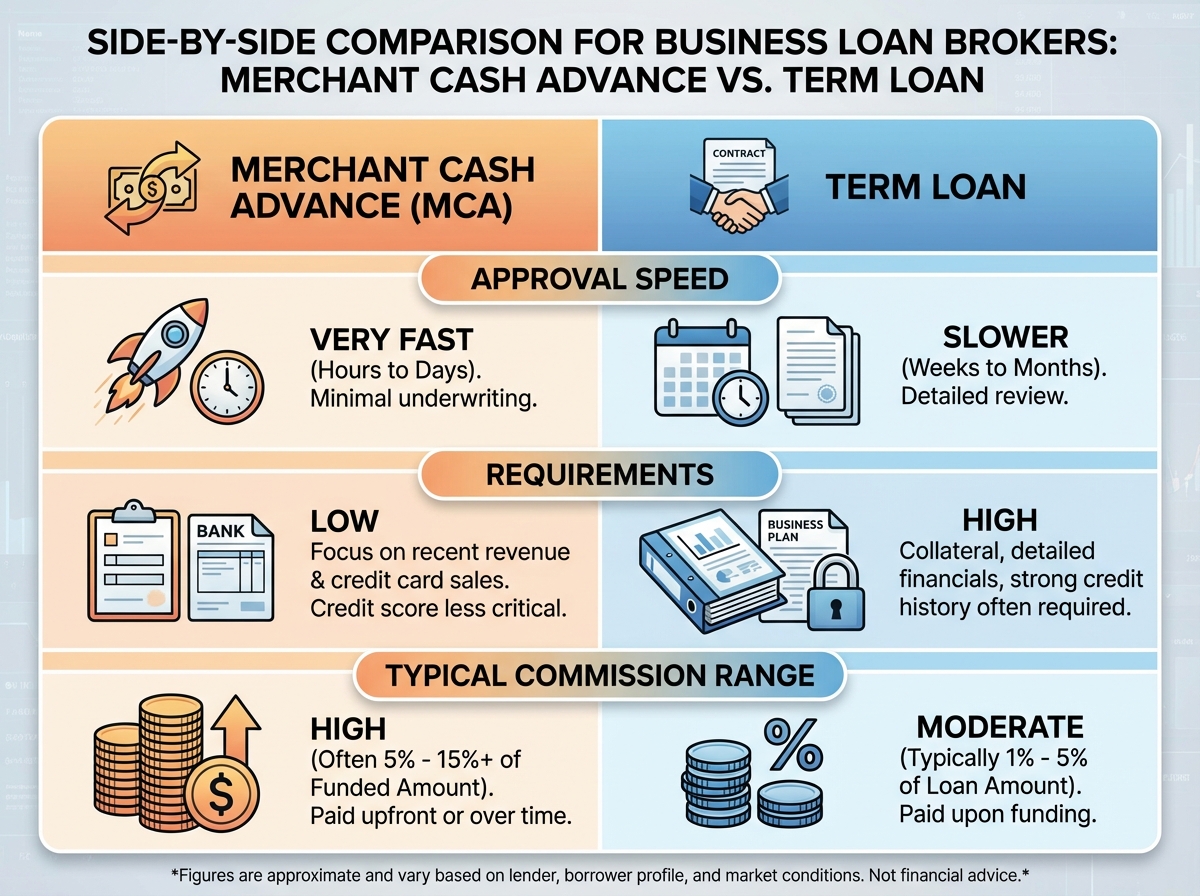

The product range is wider than most people realize when they start. Merchant cash advances (MCAs) are the most common entry point because they move fast and have looser approval requirements than traditional bank loans. But brokers also work with term loans, lines of credit, equipment financing, and 0% introductory financing products aimed at startups.

| Product Type | Typical Speed | Best For |

|---|---|---|

| Merchant Cash Advance | 24–72 hours | Businesses with consistent card sales |

| 0% Startup Financing | 1–2 weeks | New businesses needing seed capital |

| Term Loan | 1–3 weeks | Established businesses, larger amounts |

| Equipment Financing | 3–7 days | Asset-backed purchases |

Three things that will change how you see this business:

- Most small business owners have never heard the term ‘merchant cash advance’ — your job is positioning, not education

- Lenders pay you, not the borrower — which removes the most common objection before it’s raised

- Your niche matters more than your pitch — a broker who only works with restaurant owners will always outperform a generalist

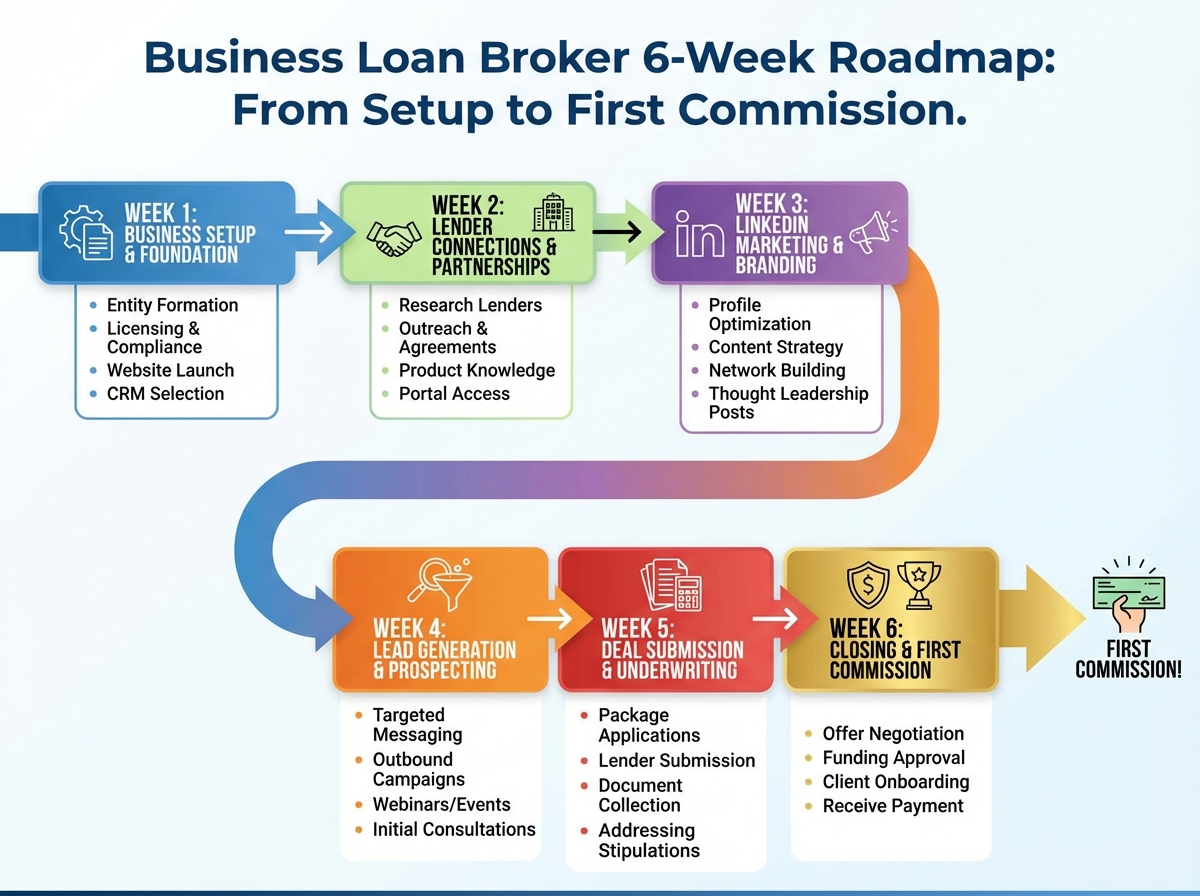

How Long It Takes to Close Your First Deal

| Stage | What You’re Doing | Time |

|---|---|---|

| Setup | Register business, connect with direct lenders, build your ISO profile | Week 1 |

| Marketing infrastructure | LinkedIn profile, Facebook group, email sequence, initial outreach | Weeks 1–2 |

| First leads | Referrals, LinkedIn connections, cold outreach responses | Weeks 2–3 |

| First submission | Qualified application submitted to a lender | Week 3–4 |

| First funded deal | Commission received | Week 4–6 |

| Total to first commission | 4–6 weeks |

Order matters more than speed here — setting up your lender relationships before generating leads means you’re never caught holding a deal with nowhere to send it. If your first deal takes eight weeks instead of four, that’s not failure — it usually means your pipeline is just starting to warm up.

The Setup Step Everyone Rushes Past

Most people who try this business and quit in the first 60 days made the same mistake: they started marketing before they had lender relationships in place. They generated interest, collected applications, and then scrambled to figure out where to send them. By the time they found a lender, the business owner had already gone somewhere else.

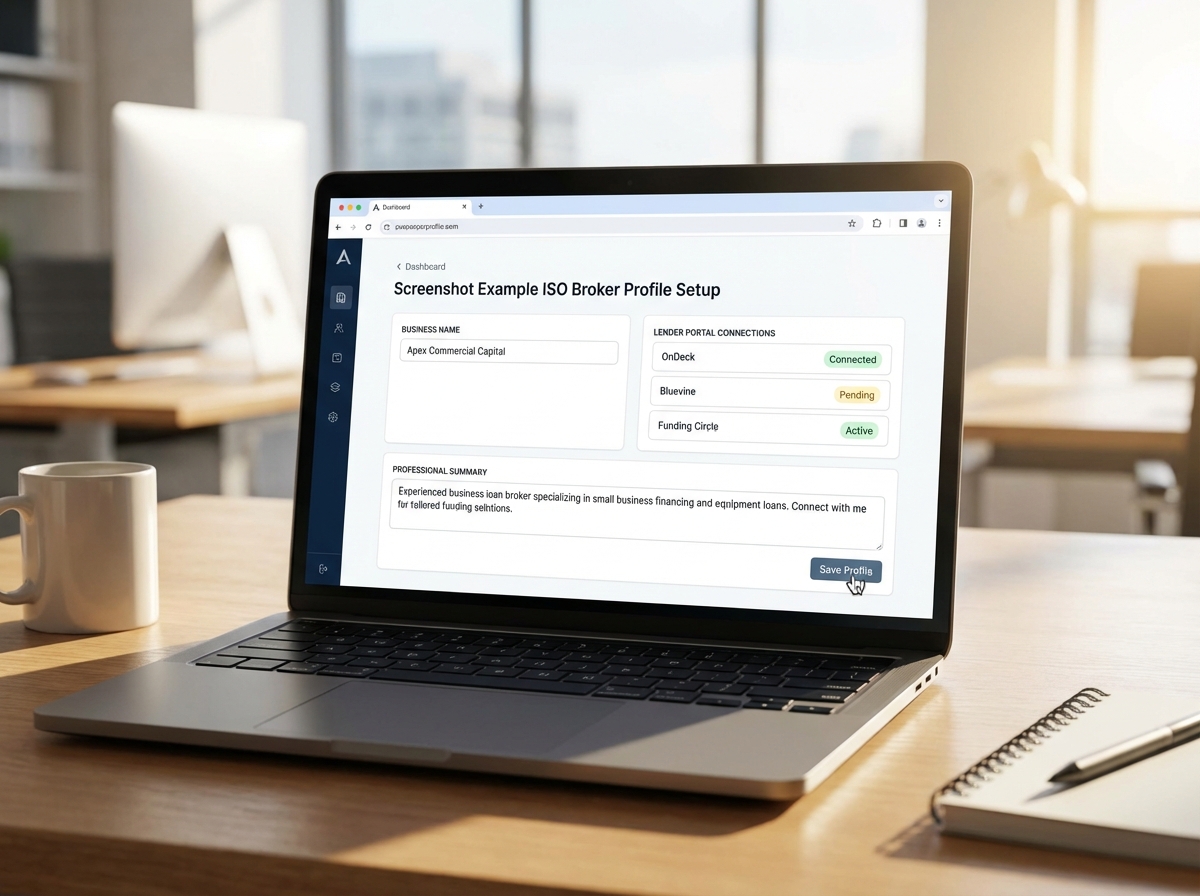

Connecting with direct lenders isn’t complicated, but it requires intentionality. You’re not just signing up for a portal — you’re building a working relationship with underwriters who will eventually prioritize your submissions because they know your deals are clean. That reputation starts from day one, with how you structure your first application.

Setting up your business entity at the same time matters for credibility. When you reach out to a business owner as an LLC or registered ISO, the conversation starts differently than if you’re reaching out as an individual with a Gmail address. The business owner is deciding whether to trust you with their financial information — presentation signals professionalism before a single word is exchanged.

The infrastructure stage feels slow because nothing visible is happening. No leads are coming in, no calls are being made. But what you’re building here — lender access, business registration, a professional presence — is the foundation that determines whether leads convert or disappear when they arrive.

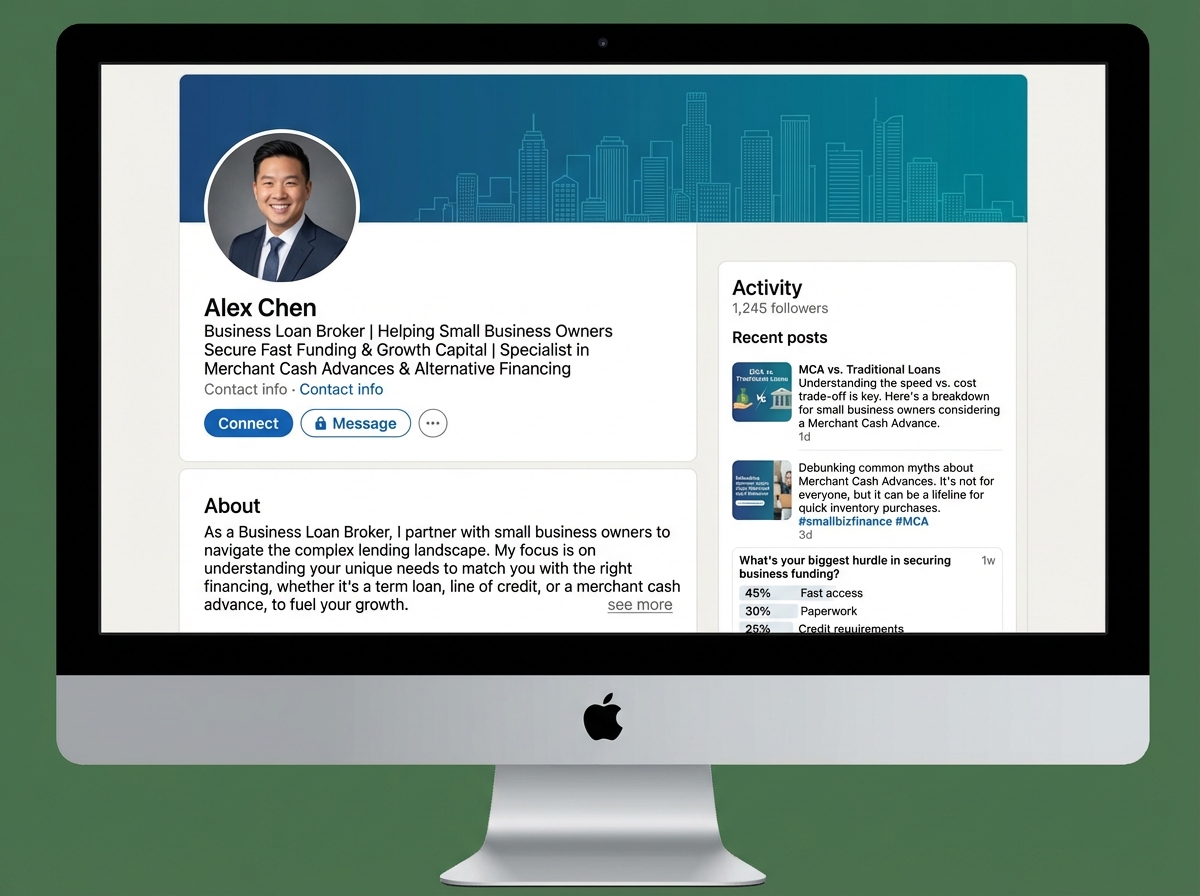

Why LinkedIn Generates the Highest-Quality Business Loan Leads

Cold outreach on LinkedIn for business loan brokering works for a specific reason that most people overlook: the platform tells you exactly what someone does before you contact them. You can see their industry, their business size, how long they’ve been operating, and whether they’re actively talking about growth or cash flow challenges. That’s intelligence you’d spend weeks building through any other channel.

The biggest mistake people make with LinkedIn as a business loan broker is treating it like a cold call list. They connect, then immediately pitch. The business owner disconnects immediately — not because they don’t need capital, but because the approach signals that you see them as a transaction, not a client. The accounts that convert are the ones that received three or four genuine engagements before a single offer was mentioned.

The LinkedIn checklist that actually moves the needle includes things like optimizing your headline so it speaks directly to business owners (not to other brokers), posting content that demonstrates you understand the problems your target niche faces, and using automation tools like DUX Soup for follow-up sequencing — not initial contact. Automation should handle the follow-up to warm connections, not the cold introduction. That distinction changes your reply rate significantly.

Once you’ve built an active LinkedIn presence, referrals start to compound on top of it. A business owner you funded six months ago mentions you to a peer. That peer looks you up on LinkedIn and sees consistent, credible content. The trust transfer is almost automatic. LinkedIn isn’t just a lead channel — it becomes a credibility anchor for every other channel you use.

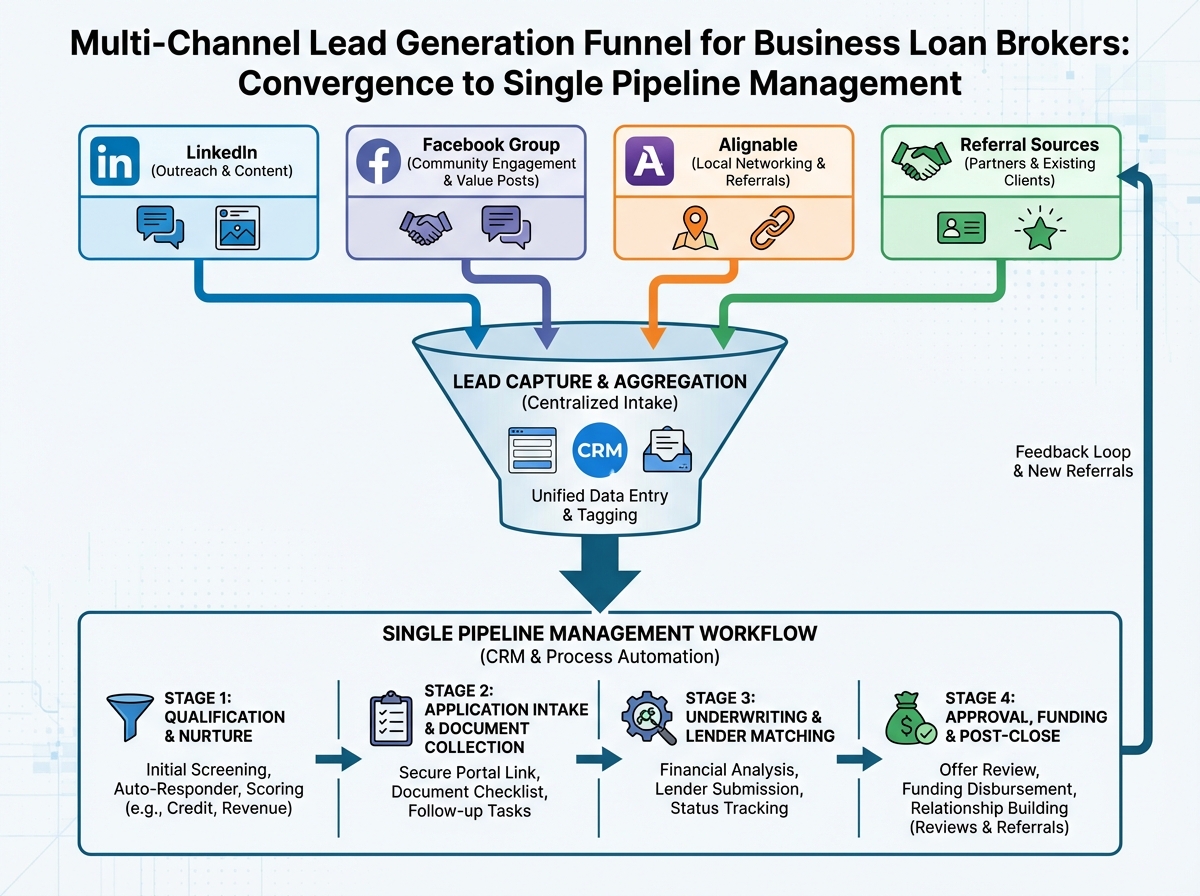

How Facebook Groups and Community Platforms Build Pipeline Over Time

LinkedIn gets you in front of professionals. Facebook groups get you in front of business owners who are already talking about their problems in public. That difference is significant. When a restaurant owner posts in a local business Facebook group asking whether anyone has experience with working capital loans, that’s not a lead you have to generate — it’s a lead that generated itself.

Building your own Facebook group is a longer play but one that pays compound returns. The group positions you as a resource, not a vendor. Business owners join because they want information. Over time, the group becomes a place where your expertise is assumed rather than asserted. Every post you make in that context lands differently than a direct message asking if they need funding.

Platforms like Alignable add another layer. Alignable is specifically designed for small business networking, which means the people there are pre-qualified by context — they’re small business owners who have opted into a business networking environment. The conversion rate from Alignable introductions tends to be higher than cold LinkedIn outreach for exactly this reason.

Buying media placements in niche publications, podcasts, or newsletters that your target business owners already read is a more advanced strategy, but it’s worth understanding early because it reframes how you think about your marketing budget. You’re not spending money on ads — you’re placing yourself in front of an audience that already trusts the channel. The leads that come in warm.

What Merchant Cash Advance Sales Actually Look Like on a Call

The first time you get a business owner on the phone who needs capital, the temptation is to explain everything — how MCAs work, what the factor rate means, how fast funding happens. That’s the wrong move. Business owners don’t want a product explanation. They want to know whether you can solve their problem, and how fast.

The script that works in this industry is built around qualification, not persuasion. You’re asking about monthly revenue, time in business, what the capital is for, and whether they’ve been declined recently. Those four questions tell you which lender to approach and how to frame the application. The selling happens through the questions, not through the pitch.

The ‘drop’ technique — following up immediately after an application goes to a lender — keeps the business owner engaged during the wait period and positions you as an advocate rather than an intermediary. Business owners who feel like someone is actively working their file are less likely to go shop their application elsewhere while you’re waiting for approval. That alone protects a significant portion of your pipeline from leaking.

Closing in this business is largely about removing friction, not creating urgency. Urgency is already there — the business owner has a problem they need money to solve. Your job is to make the paperwork feel manageable, the timeline feel real, and the lender feel trustworthy. When all three of those things are true, the close isn’t a close — it’s a natural next step.

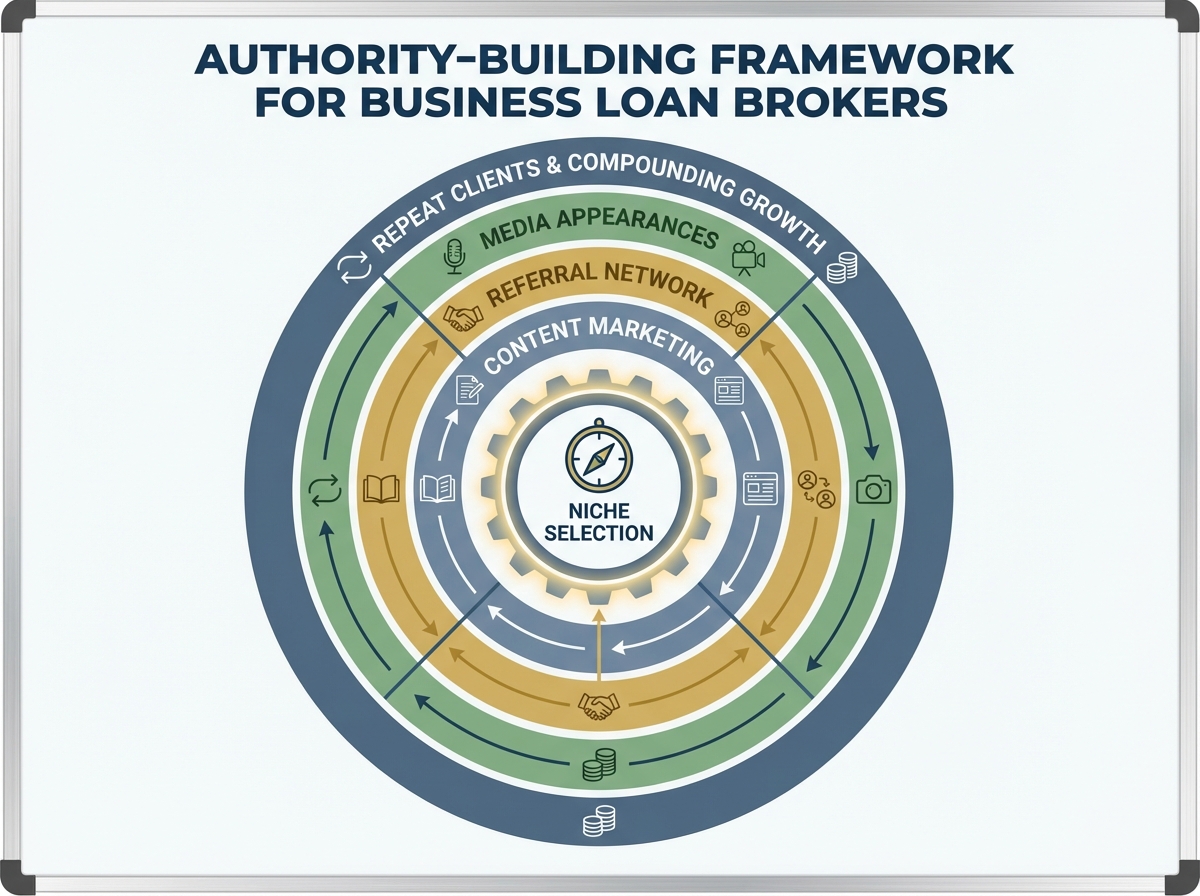

Becoming an Authority in a Niche Instead of Chasing Everyone

The brokers who struggle are almost always generalists. They’ll work with any business, in any industry, at any stage. That sounds like maximum opportunity, but it operates like maximum noise. No clear message, no referral network, no compounding credibility.

Picking a niche — restaurants, medical practices, trucking companies, real estate investors — changes everything. You start to know the seasonality of that industry’s cash flow problems. You know what lenders are most favorable for that sector. You know what language the business owner uses to describe their situation, which means your outreach sounds like it was written for them specifically, because it was.

Becoming an authority doesn’t require a podcast or a book. It requires showing up consistently in the channels your niche uses and demonstrating that you understand their business before they’ve told you anything about it. Doing interviews for industry podcasts or local business publications is one of the fastest ways to compress that timeline — being quoted as an expert in a publication that a business owner already reads builds more credibility in five minutes than six months of cold outreach.

Branding is a downstream consequence of authority, not a prerequisite for it. The mistake is trying to build a brand before you’ve built a track record. Your brand eventually becomes: the broker who specializes in [niche], who closes fast, who doesn’t waste your time. That reputation builds itself once you’re working consistently. What you control early is the niche and the channels — the brand follows.

What Actually Makes This Business Work Long-Term

Looking back at the whole arc of this — from the first confused Google search about how loan brokering actually works, to having a functioning pipeline with repeat referrals — the thing that mattered most wasn’t the product knowledge or even the sales script. It was lead volume, and specifically, the consistency of lead generation across multiple channels running simultaneously.

When only one channel is working, the business feels fragile. One algorithm change, one slow month on LinkedIn, one dried-up referral source — and the pipeline stalls. When three or four channels are running in parallel, slowdowns in one are invisible in the aggregate. That’s the infrastructure goal. Not perfection in any single channel, but redundancy across all of them.

Here’s what to do as soon as you finish reading this:

- Register your business entity before anything else — even a simple LLC signals professionalism and is required to work with most direct lenders

- Connect with at least three direct lenders in your first week — having multiple options means you can shop a deal for the best approval rather than being stuck with one decision

- Optimize your LinkedIn headline for your target niche — replace generic phrases like “financial professional” with something specific: “Funding solutions for [industry] businesses”

- Start a Facebook group around a problem your niche has — not around your service, around their pain point; the group becomes a long-term inbound engine

- Build your qualification script before your pitch — knowing what four questions to ask on a first call will close more deals than any persuasion technique

- Choose one niche and commit to it for 90 days — generalism feels safe but produces weak results; specificity feels risky but compounds quickly

- Follow up every submitted application the same day it goes to a lender — the drop technique is not optional; it protects deals that would otherwise shop themselves out while waiting

- Track which channel each lead came from — not to optimize immediately, but to know which channels to double down on once your first five deals close

Leave a Reply