The first time someone explained Bitcoin to me, I nodded along and understood nothing. Not because it’s complicated — but because the explanation started in the wrong place.

If you’re looking to learn Bitcoin, the fastest way in is to stop treating it like a technology problem and start treating it like a money problem. Bitcoin is not about code. It’s about what money is, why the current system fails ordinary people, and what a fixed-supply, decentralized alternative actually means for your savings. Once that reframe clicks, everything else — the wallets, the keys, the blockchain — stops feeling like jargon and starts feeling like tools.

- Bitcoin matters most to people who’ve already felt inflation quietly drain their savings account

- Understanding the investment thesis comes before understanding how to buy

- Self-custody — holding your own keys — is what separates owning Bitcoin from just having a number on an exchange screen

What Bitcoin Actually Is (Not the Tech Explanation)

Most beginner explanations of Bitcoin reach for the blockchain within the first two sentences. That’s the wrong move. Before any of that, you need a working definition that’s honest about what Bitcoin is trying to replace.

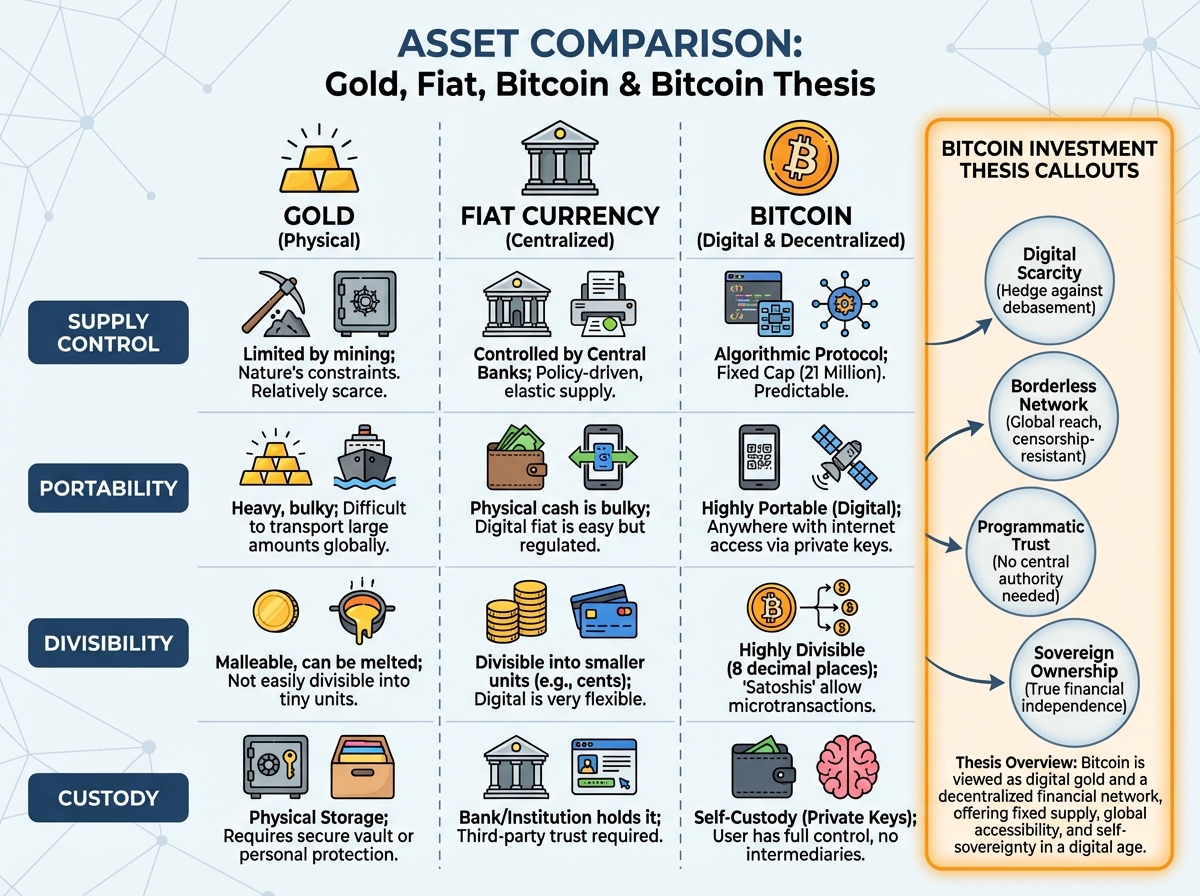

Bitcoin is a fixed-supply digital currency with a hard cap of 21 million coins, secured by a decentralized network with no central issuing authority. Unlike dollars, euros, or any government-backed currency, no one can print more of it. That scarcity is the entire foundation of the argument that it works as a store of value — the way gold has functioned for centuries, except Bitcoin is portable, divisible down to a hundred millionths of a coin (called a satoshi), and transferable without a bank.

Here’s a quick frame for how Bitcoin sits relative to the things people already understand:

| Thing | What It Is | Bitcoin Comparison |

|---|---|---|

| Gold | Scarce physical asset, store of value | Bitcoin is often called “digital gold” — same scarcity logic, none of the physical logistics |

| Cash | Government-issued, spendable anywhere | Bitcoin is spendable globally, but not issued or controlled by any government |

| Bank account | Your money held by someone else | Bitcoin held in self-custody means no intermediary can freeze or inflate it |

| Stock | Ownership stake in a company | Bitcoin represents no ownership — it is the asset itself |

The definition that matters for a new investor is this: Bitcoin is a bet that scarcity still means something in a world where every government currency is being inflated.

Three Things That Surprised Me About Bitcoin Early On

- Bitcoin has never been successfully hacked at the protocol level — breaches always happen at the exchange or wallet layer

- The biggest early adopters weren’t tech libertarians — they were people in countries with collapsing currencies

- You don’t have to buy a whole Bitcoin — most people start with whatever they can afford, measured in satoshis

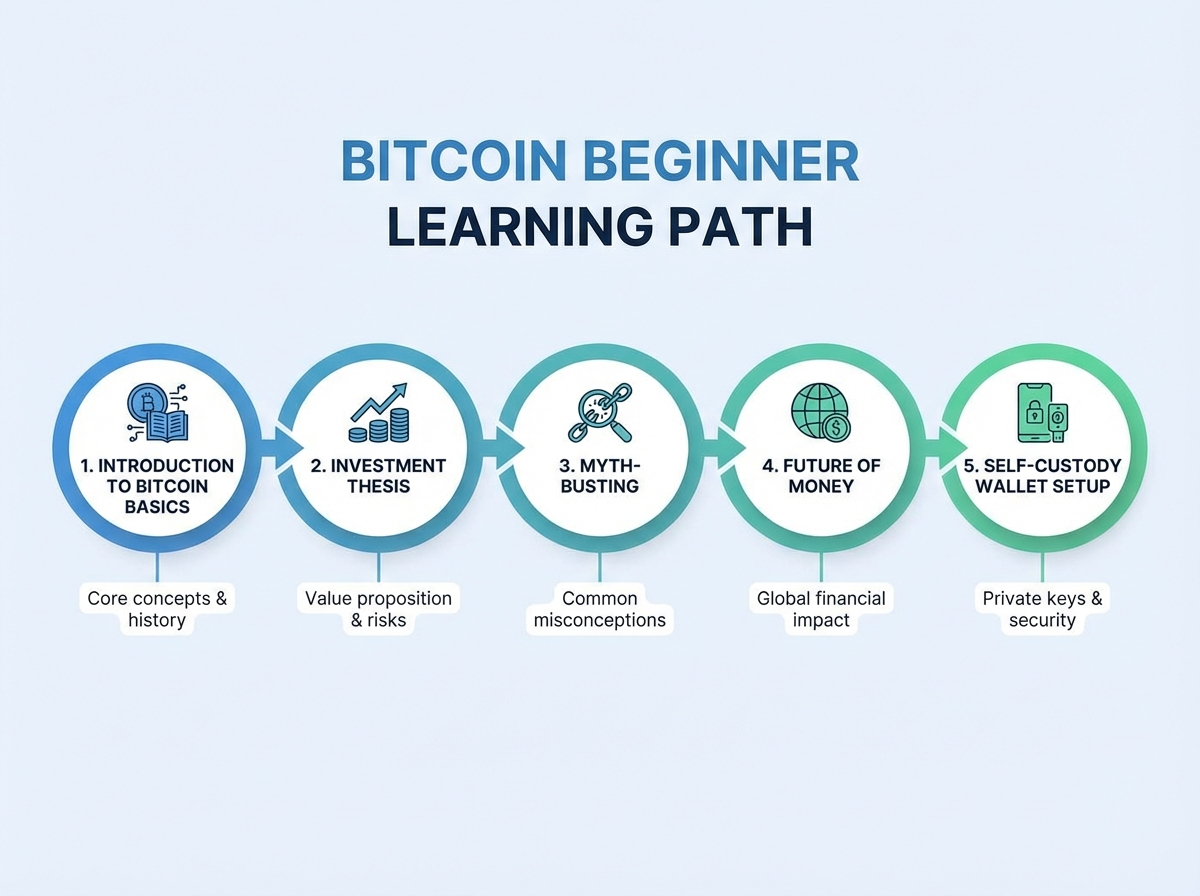

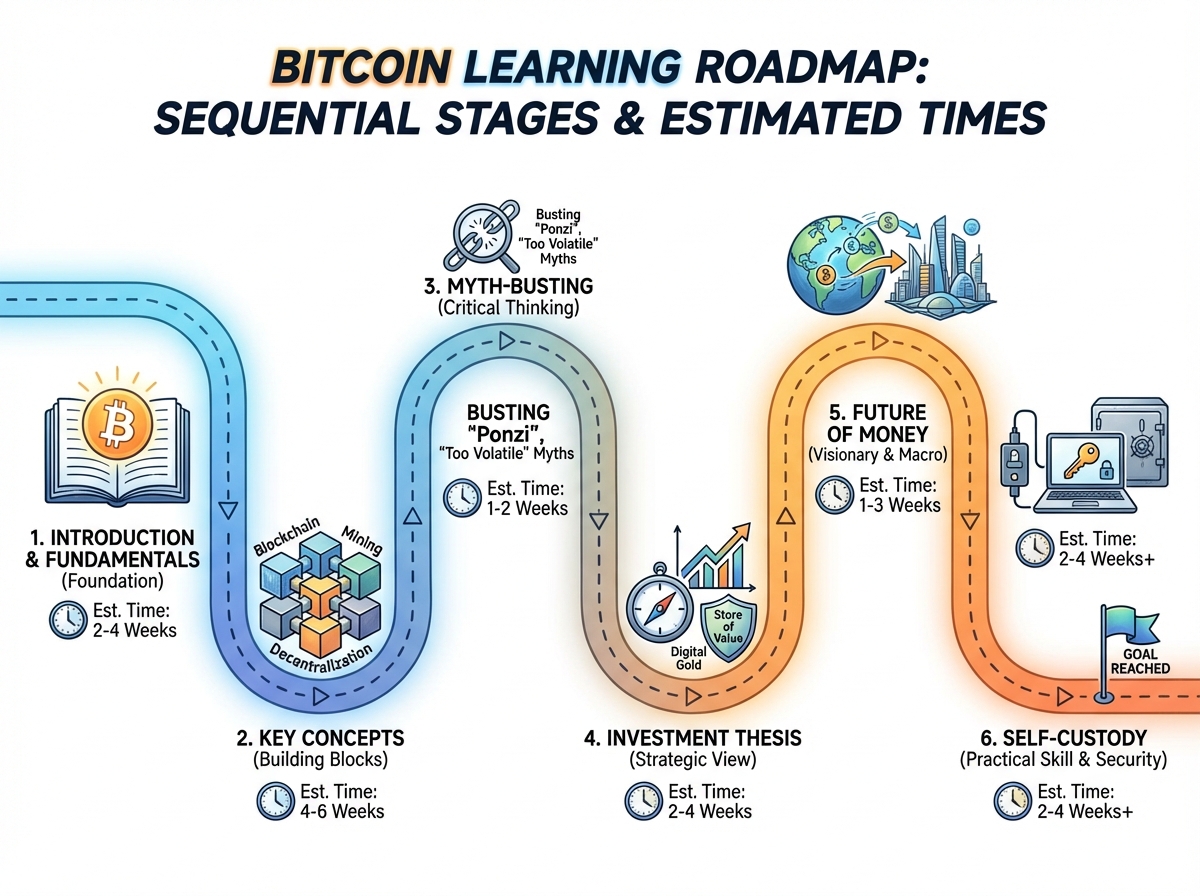

How Long Does It Take to Actually Understand Bitcoin?

| Stage | What You’re Working Through | Estimated Time |

|---|---|---|

| What is Bitcoin? | Core concept, how it differs from fiat, why it exists | 15–20 minutes |

| The investment thesis | Scarcity, inflation hedge, store of value case | 10–15 minutes |

| Myth-busting | Energy use, government bans, scam narratives | 10 minutes |

| The future of money | Why the current monetary system is broken | 10 minutes |

| Key concepts recap | Blockchain basics, wallets, private keys reinforced | 8–10 minutes |

| Self-custody and freedom money | Hardware wallets, cold storage, taking possession | 5–10 minutes |

| Total | Full conceptual foundation | ~1 hour |

The order matters more than the pace — trying to understand self-custody before you understand why Bitcoin exists produces exactly the confusion that makes people quit. If you take longer than an hour, that’s fine. Sitting with the inflation and scarcity argument until it genuinely makes sense to you is worth more than rushing to the wallet setup.

The Moment the Investment Thesis Actually Clicks

The investment thesis for Bitcoin sounds abstract until you connect it to something you’ve personally felt. Most people have had the experience of watching prices rise year over year — groceries, rent, anything — while their savings account pays 0.5% interest. That gap is inflation doing exactly what it’s designed to do in a fiat system: quietly redistributing purchasing power away from savers.

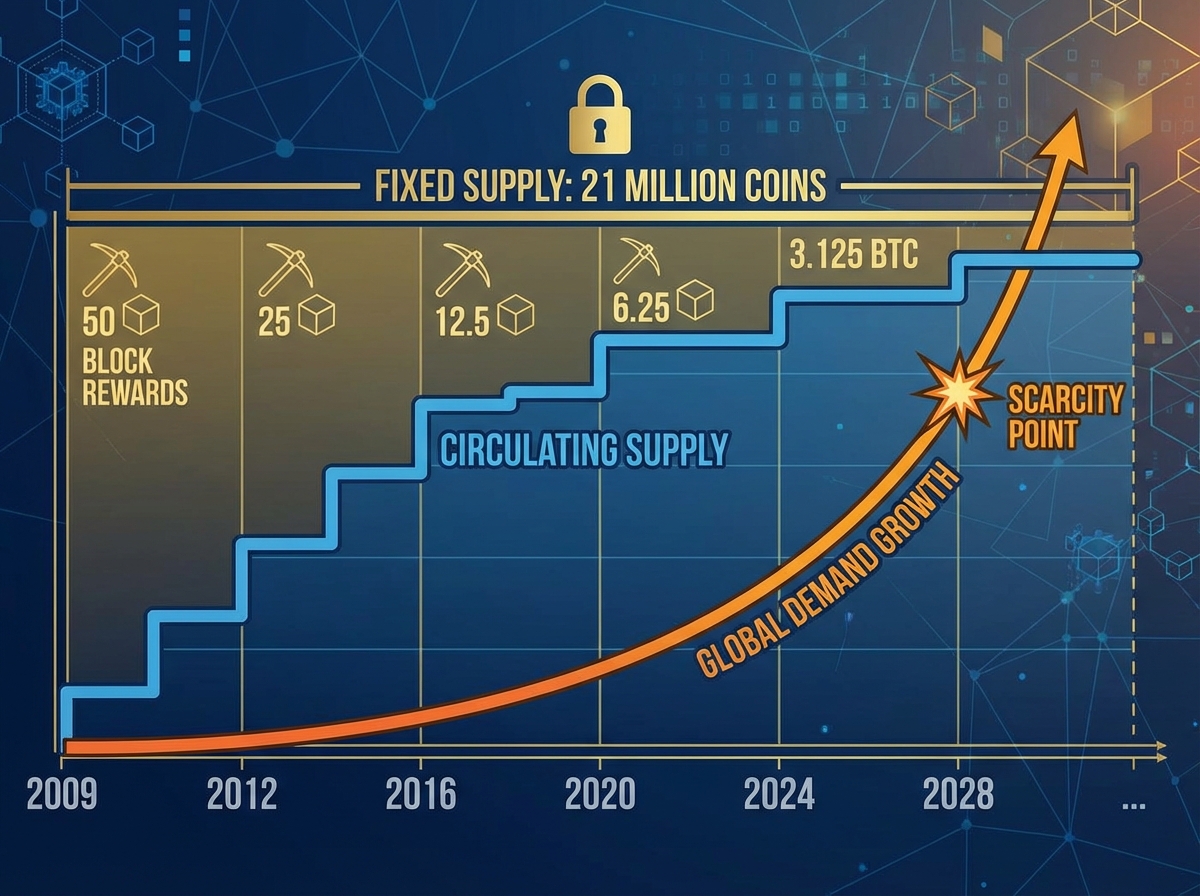

Bitcoin’s counter-argument is simple. There will only ever be 21 million Bitcoin. Miners who validate transactions receive newly issued Bitcoin as a reward, but that reward halves roughly every four years — an event called the halving — until issuance reaches zero. By design, demand can grow while supply stays fixed. That’s the opposite of how every government currency works.

The thesis is not that Bitcoin will replace the dollar tomorrow. The thesis is that as more individuals, institutions, and eventually governments allocate even a small percentage of their holdings to Bitcoin — the way a portfolio manager might allocate 3–5% to gold — the demand pressure on a fixed supply pushes value upward over time. That’s it. That’s the whole argument. The rest of the noise — price predictions, short-term volatility, headlines — is largely irrelevant to the thesis.

Why the Myths Hit So Hard Before You Know Better

The biggest mistake people make when learning Bitcoin is Googling it before they have any grounding in the investment thesis. The search results are a mix of genuine skepticism, well-intentioned but outdated concerns, and active disinformation — and without a framework, it all sounds equally credible.

The most common myths follow a pattern: they take a real feature of Bitcoin and misrepresent its significance. Bitcoin does use energy — but so does every other payment system, including the data centers that run Visa and Mastercard, plus the physical bank branches, ATMs, and armored trucks behind them. When you compare the full energy footprint of the traditional banking system to Bitcoin’s network, the picture is considerably more complicated than “Bitcoin bad for environment.” The nuance is real, but the conclusion most people arrive at from headlines is not.

The government ban argument is another persistent ghost. Governments have the ability to restrict exchanges within their borders — they can make Bitcoin harder to buy through regulated channels. They cannot delete Bitcoin. The network runs on nodes distributed globally, no single one of which can be shut down to stop the whole thing. China has “banned” Bitcoin multiple times and yet China-based mining operations continued operating under different structures. The network didn’t notice.

The Broken Money Problem Nobody Talks About

There’s a section of the Bitcoin conversation that most introductions skip entirely because it sounds too political: the argument that our current monetary system is structurally broken for ordinary people. Not broken in a conspiracy sense — broken in a measurable, documented, thoroughly boring accounting sense.

Since the U.S. abandoned the gold standard in 1971, the dollar has lost over 85% of its purchasing power. Central banks can and do expand the money supply in response to crises — 2008, 2020 — and while that stabilizes financial systems in the short term, the long-term effect lands disproportionately on people who hold cash savings rather than assets. If you own property, stocks, or gold, inflation mostly pushes those asset prices up with it. If you hold cash, you just get poorer in slow motion.

Bitcoin’s response to this isn’t ideological in the sense of being anti-government. It’s structural. A currency that no one can inflate is a different kind of savings instrument than anything that has existed since the gold standard ended. Whether Bitcoin achieves that vision at scale is genuinely uncertain — but the problem it’s trying to solve is not a myth. The problem is real, documented, and worth understanding before you form an opinion about whether Bitcoin is a solution to it.

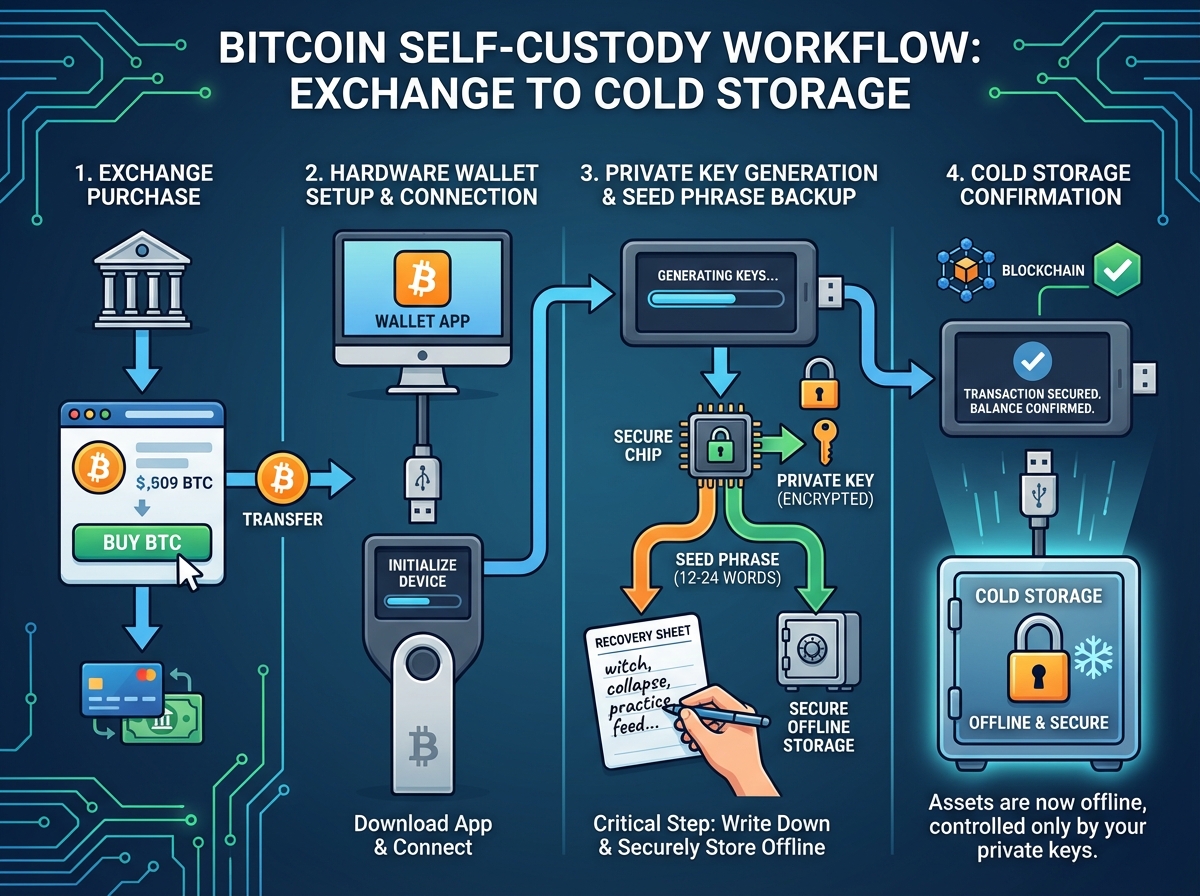

What Self-Custody Is and Why It Changes Everything

At some point in the Bitcoin education journey, the phrase “not your keys, not your coins” will appear. It sounds like a slogan. It’s actually the most practically important concept in the entire space.

When you buy Bitcoin through an exchange and leave it there, you don’t hold Bitcoin in the way that Bitcoin was designed to be held. You hold an IOU. The exchange holds the actual Bitcoin and has the cryptographic keys that control it. That’s fine for trading. It is not fine for a long-term store of value position, because exchanges can be hacked, can freeze withdrawals, can go insolvent — as FTX did in 2022, taking billions in customer funds with it.

Self-custody means moving your Bitcoin off an exchange into a wallet where only you hold the private keys. A hardware wallet — a small physical device that stores your keys offline — is the standard recommendation for any holding you intend to keep for years. The setup takes under an hour. The seed phrase — a sequence of 12 or 24 words — is your backup. Anyone who has that phrase can access your Bitcoin. No one who doesn’t have it can. That asymmetry is the freedom part of “freedom money.” You can send value anywhere in the world without asking anyone’s permission.

The Bitcoin Learning Mistake That Costs People Real Money

The most expensive mistake in the early Bitcoin learning curve isn’t buying at the wrong time. It’s skipping the self-custody education entirely. Most people who lose Bitcoin don’t lose it because the network was hacked. They lose it because they left it on an exchange that failed, lost access to a wallet they didn’t properly back up, or handed the seed phrase to someone who asked for it. Every one of those is a preventable error, and every one of them comes from treating Bitcoin like a stock — something you buy, leave somewhere, and check on periodically — rather than a bearer asset that requires you to actually hold it.

The other mistake is less dramatic but just as common: people research Bitcoin in a mood. They find it during a price spike, get excited, buy something, watch the price drop 40%, and interpret that as confirmation that it was a scam all along. Bitcoin has had multiple 80%+ drawdowns across its history and has recovered each time to make new highs. The people who lost money permanently were the ones who sold during the drawdown because they never actually understood what they owned.

What Changes After You Actually Understand Bitcoin

Something shifts when the investment thesis for Bitcoin genuinely lands — not just intellectually but as something you can explain to someone else in plain language. The noise level drops. The headlines about price become less interesting. The question stops being “should I buy Bitcoin” and starts being “how much of my savings should I hold in something that can’t be inflated, and how do I hold it properly.”

That’s the shift from speculator to holder. Speculators trade the price. Holders understand the asset. The people who have consistently done well in Bitcoin over multi-year periods are almost entirely in the second category — not because they were lucky, but because they understood clearly what they owned and why they owned it, well enough not to sell during the inevitable volatility.

The education that gets you there doesn’t have to be long. The core concepts — scarcity, inflation hedge, self-custody, the investment thesis, debunking the main myths — can be absorbed in about an hour. What takes longer is the sitting with it, questioning it, and eventually arriving at a personal conviction about whether it fits your financial picture. But you can’t have that conviction without the foundation.

Before You Buy: Actionable Steps That Actually Matter

Understand what Bitcoin is solving before you buy any. The price action means nothing if you don’t have a thesis — without one, every dip will feel like a reason to sell and every spike will feel like you missed it.

Learn the difference between a hot wallet and a cold wallet. Hot wallets are connected to the internet; cold wallets (hardware wallets) are not. For any amount you’d be upset to lose, cold storage is the standard.

Write your seed phrase on paper and store it physically, not digitally. Screenshots, cloud notes, and email drafts are all ways people have permanently lost access to their Bitcoin. Physical paper in a safe location is still the best practice.

Start with a small amount — less than you’d spend on a dinner out. The goal of the first purchase is to go through the full experience of buying, transferring to a wallet, and verifying the balance. The learning value comes from doing it, not from the amount.

Don’t check the price daily. Bitcoin’s daily and even monthly volatility is high. If you’re holding as a long-term store of value, frequent price-checking creates psychological pressure to make decisions based on noise rather than thesis.

Research the halving cycle before forming a price opinion. Bitcoin’s issuance halves roughly every four years. Historically, the halving has preceded significant price appreciation 12–18 months later — not guaranteed, but structurally relevant to any multi-year hold.

Choose a regulated exchange with strong security for your initial purchase. Coinbase, Kraken, Gemini, and River are commonly cited for their security practices and regulatory compliance in the U.S. market. Check what’s available and regulated in your country.

Learn to verify a receive address before you transfer anything. A single character error in a Bitcoin address sends funds permanently to the wrong destination with no recourse. Always verify the first and last four characters of any address before confirming a transaction.

Leave a Reply